Pro-Demnity is dedicated to upholding fairness and integrity in our pricing and ensuring that premiums are priced equitably, in accordance with every architectural practice’s claim history. Understanding how your professional liability insurance premium is calculated can help you to manage your business and plan or forecast with confidence.

In 2025 the Experience Rating Factor (ERF, or Experience Adjustment Factor), a loss ratio measure by policyholder against Pro-Demnity’s loss ratio, is being integrated into the existing premium calculation.

Below is a simple illustration of how the ERF impacts premiums at the minimum mandatory level of coverage of $250,000 per claim.

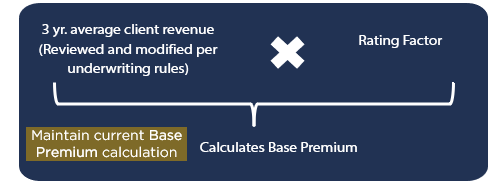

Step 1: Average out three years Gross Fees

The average of the three most recent years of gross fees for an architectural practice are always used. This approach minimizes and smooths out large swings – either upwards or downwards – that a firm might experience, year over year. This favours all firms, whether they are experiencing downturns followed by growth bursts, and vice versa.

Let’s assume that a fictional architectural firm, ZZZ Architects Inc., reported their fees as follows:

Fees reported for 2023 renewal: $250,000

Fees reported for 2024 renewal: $200,000

Fees reported for 2025 renewal: $150,000

Their 3-year average revenue (2023 – 2025) is: $200,000

Step 2: Multiply the 3-year average of Gross Fees by the Annual Rating Factor (or rate increase) to calculate the Base Premium

The 3-year average revenue is then multiplied by the Rating Factor (or Rate Increase) which is applied to every practice (regardless of individual claims history) annually upon renewal. The rating factor provides additional capital cushion to the entire book of business in the event of severe and catastrophic claims. Over the past seven years the rate increase has been between 1 % and 5 %. We encourage firms to consistently budget for 5 % increases in their financial planning scenarios and budgets annually.

From April 1, 2025, to March 31, 2026, the rate increase is 4 %.

This multiplication above, will yield the Base Premium as follows:

$200,000 (3-yr avg revenue) x 4 % (rate increase) = $8,000 (base premium)

This is the Base Premium for the practice upon renewal. Depending on the practice, there may be other applicable relative adjustments for deductibles, limits, etc., that will continue to apply.

Step 3: Loss Ratios as inputs to the Experience Rating Factor

The Experience Rating Factor (ERF) represents the firm’s loss ratio (severity of claims) over a period of 10 years as compared against Pro-Demnity’s equivalent loss ratio for the same period of time.

For the 2025 ERF, the 10-year period is 2013-2022, reflecting claims losses incurred for that duration of time as of December 31, 2024. Any recent claims incurred in 2023 to 2024 are excluded from the 2025 premium calculation year because claims are unpredictable and fluctuate in their first two years. This exclusion is in the firm’s favour and provides them with sufficient time to plan for a stable potential surcharge in premiums in future years.

The ERF for ZZZ Architects Inc. is unique to them and reflective of claim costs (paid expenses, or damages or both) based on severity and NOT the number of claims reported or actioned. We exclude all paid claims less than $5,000 in this calculation.

So, we need to identify two loss ratios: that of Pro-Demnity’s and that of the firm’s for the same 10-year period. If the firm’s loss ratio is higher than Pro-Demnity’s, they will experience a surcharge on their premium. If lower, it will be a discount to their premium.

Let’s assume that Pro-Demnity’s loss ratio is 60 % and ZZZ Architects Inc.’s loss ratio is higher, at 75 % for the same 10-year time frame. After adjustments, the firm’s Experience Rating Factor is 1.0700.

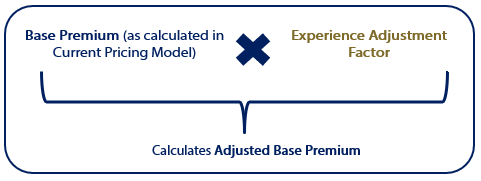

Step 4: Multiply the Base Premium with the Experience Rating Factor to calculate the Adjusted Base Premium

In the case of ZZZ Architects Inc., their Base Premium is then multiplied by the firm’s Experience Rating Factor (ERF) to determine their Adjusted Base Premium, which reflects a discount or a surcharge on their premium for the year.

Base Premium x Experience Rating Factor = Adjusted Base Premium

$8,000 (base premium) x 1.0700 (ERF) = $8,560 as the Adjusted Base Premium.

ZZZ Architects Inc., would therefore have experienced a 7 % premium surcharge.

Let’s now imagine a scenario where ZZZ Architects Inc.’s loss ratio was lower than that of

Pro-Demnity’s in Step 3 above and that it was 53%. After adjustments, the firm’s Experience Rating Factor is 0.97.

Base Premium x Experience Rating Factor = Adjusted Base Premium

$8,000 (base premium) x 0.97 (ERF) = $7,760 as the Adjusted Base Premium.

ZZZ Architects Inc., would therefore have experienced a 3 % premium discount.

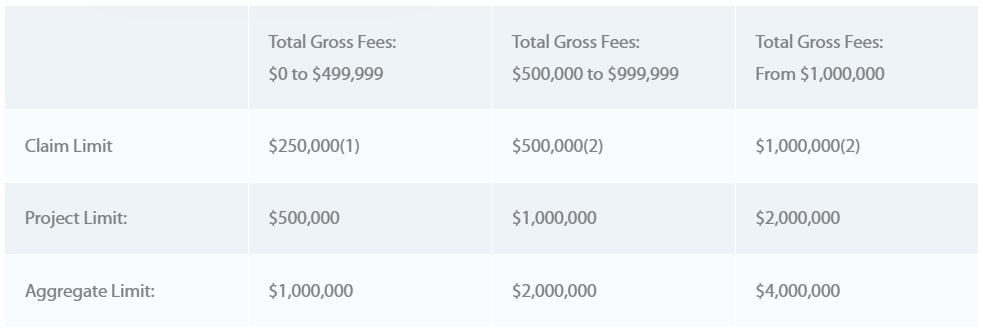

The Impact of Increased Mandatory Limits on Premium

As your architectural practice grows, so too will your mandatory limits of liability, and consequently, your premium.

For example, when reported gross fees are over $500 K or $1 M, the mandatory Claim, Project and Aggregate Limits also increase commensurate with your firm’s growth (see the chart below). The jump to the next mandatory tier, triggers an increase in premium.

For increased limits premiums, the formula calculations begin the same way as steps 2, 3 and 4 above. However, there are additional inputs and factors specific to increased limits as well as further adjustment factors applied by reinsurers, to arrive at a Total Adjusted Premium.

Should you require a more detailed explanation specific to your firm, please reach out to our Underwriting team after you’ve received your renewal package.