The Straight Line Newsletter — Issue #2

Welcome to the 14th issue of The Straight Line, now a quarterly. Why quarterly? Because things in general – liability insurance in particular – seem to be changing more rapidly than ever, even as many of us, stuck in our makeshift home offices, watch time slowly stroll by.

In This Issue

What limits should I carry? Mandatory limits changed Serving on a Condominium Board

This is the second issue of The Straight Line, a newsletter that will appear occasionally throughout the year. Articles will cover a broad range of topics that will engage anyone with an interest in the profession, including Ontario architects insured by Pro-Demnity, other OAA members— whether in practice or engaged in other businesses—and others.

We encourage readers to suggest topics for future issues of The Straight Line. Please send any suggestions to: mail@prodemnity.com

New Chair at Pro-Demnity

At the recent Pro-Demnity Annual General Meeting, Bill Birdsell was elected to the Board and appointed as the new Chair. Chris Fillingham, the retiring Chair of Pro-Demnity, has assumed the role of Director Emeritus for the coming year to assist with the transition. Bill served on OAA Council for seven years, including two terms as President. During his time on Council, Bill was appointed to the Pro-Demnity Board as an OAA designate for several terms. He has been a champion of strengthened understanding of the role of Pro-Demnity throughout the profession and at Council.

— The Editor

Pro-Demnity is regularly asked by architects to suggest what would be appropriate claim limits for their practice. There is no single answer or formula that applies, and every architect must reach its own conclusion reflecting its own circumstances. Mario Delgado, a lawyer experienced in defending claims against architects, offers his observations.

Before finalizing an agreement with a prospective client, architects should consider whether they carry sufficient coverage.

All architects with a Certificate of Practice are legally required to have stipulated minimum limits of professional liability insurance unless exempted. But sometimes, the amount of coverage is imposed on the architect as a condition of engagement. In other cases, the amount of professional liability coverage may be negotiated with the client. Where a client does not have its own requirements, the option of higher limits is left to the architect’s discretion.

In this article we discuss the wisdom of relying on the minimum coverage and limits, and point out some of the problems that may arise if this issue is given insufficient thought.

What are the Mandatory Limits?

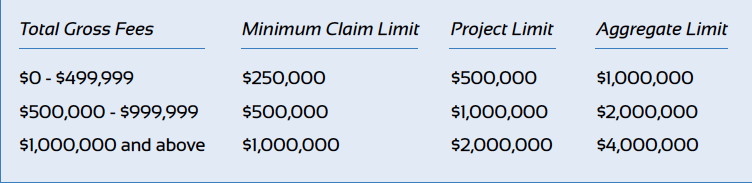

Effective January 1, 2016 the Ontario government approved changes to the Mandatory Limits of Liability required to be maintained by architects. Three levels of mandatory limits now apply, depending on gross fees received and reported by the practice for the prior year, as illustrated on the chart below:

Claim Limit is the maximum amount the Insurer will pay as Damages for each Claim during the Period of Insurance.

Project Limit is the maximum amount the Insurer will pay as Damages for all Claims during the Period of Insurance arising from the performance of professional services with respect to one project, subject always to the Claim Limit of Liability for one Claim.

Aggregate Limit is the maximum amount the Insurer will pay as Damages for all Claims during the Period of Insurance, subject always to the Claim Limit of Liability for one Claim and the Project Limit of Liability for all Claims with respect to one project.

Refer to Pro-Demnity’s Professional Liability Insurance Policy for complete policy wording describing Limits of Liability.

Ask an Expert

“Ask an Expert” offers readers the opportunity to obtain advice from members of a panel of experts familiar with architectural practice and insurance considerations. Questions will be selected that illustrate legal and insurance issues and principles that apply broadly in practice, while ensuring that specific individuals, projects and circumstances cannot be identified.

Answers provided will be general in nature and cannot be taken as legal or insurance advice for readers to apply to their own circumstances. Please consult your own lawyer or Pro-Demnity with respect to any questions or concerns impacting your own practice. Questions should be directed to: riskmanagement@prodemnity.com

An Ontario architect poses a question: I am an Ontario architect. I’ve been asked if I would consider joining the board of directors of the condominium in which I live. What can I do to protect myself from liability as an architect while best serving the condominium corporation?

Rachel Migicovsky of Shibley Righton LLP offers this advice: Architects are frequently approached

by the condominium boards to join as directors. It seems like a win-win for the board and for the architect: the board may think it gets an architect to give them free advice on important decisions; the architect gets to build her profile. However, it is important for the architect to take precautions. See below for more detail.

Manage Expectations

There are no problems with the architect joining the board as a unit owner. However, the architect must remember that she is on the board in a personal and not professional capacity. The architect must ensure that she does not present herself as an “in-house architect” and that the other board members do not treat her as one. This may involve explicit reminders from time-to-time, and the architect should be prepared to step aside if the board members don’t get the message. This is important: architects must protect themselves and not take any steps that might interfere with their insurance coverage.

In this respect: Understand the Insurance

Architects are not covered by their Pro-Demnity Insurance Company Professional Liability Insurance Policy (the “Policy”) when acting as a director of a condominium corporation. Under Part III(1)(g) “Exclusions”, the Policy says that Pro-Demnity will not cover the architect for claims arising out of “the performance of services not usual or customary for holders of certificates of practice, or members of the [OAA]” i.e. the architect is not covered for providing services to the condominium that are not architectural and not provided through its certificate of practice.

However, a condominium corporation should (and most do) offer Directors and Officers insurance coverage to protect their directors in the event of claims against the condominium corporation. The architect should be certain to review that policy and find out what she is and is not covered for. In certain circumstances the directors of a corporation can be held personally liable for wrongdoing by the corporation, and the architect sitting on the board of a condominium corporation should be protect-ed by insurance against that eventuality.

The Condominium Act, 1998, 1998 S.O. c. 19, s. 39 says that the condominium corporation shall purchase and maintain insurance for the benefit of a director or officer where the insurance is “reasonably available.” The Condominium Act does not define when coverage is “reasonably available.” The architect should confirm that coverage is in place before agreeing to join the board of directors.

Conflicts of Interest

There can be issues where an architect is a director and also accepts a retainer for a project relating to the condominium. Residents and other board members may perceive the architect to be acting in her own self-interest for accepting the retainer, and may be seen to be putting her own interests ahead of those of the condominium. Directors of corporations owe fiduciary duties to the corporations, which means they must always act in the best interest of the corporation. The test is not whether the architect has placed her own interest above that of the corporation, but whether there is the appearance of a conflict. If the architect is seen to place her own interest above that of the corporation, then she is in a conflict of interest.

The architect should not offer her services as architect to the corporation, if she is also a director, and should be cautious about making recommendations with respect to architects when hiring for a particular project. If the board decides to retain an architect for a project, the architect should consider abstaining from the vote, or even the entire process.

Provided an architect does not place herself in a position of conflict, she can serve on a condominium corporation’s board of directors and provide a benefit to the condominium.

— Rachel Migicovsky

Letters to the Editor

Dear Straight Line:

What a surprise, or rather shock it is to read your suggestion that architects should ask their client “what steps it will be taking to address the life safety issues.”

Though it is our obligation (both professional and moral), to make our clients well aware of any health or life safety issues that one encounters during a requested review, or accidental for that matter, why would an Architect, its governing body or insurer wish to take on the role of “Policeman”? Once the question is asked, there is no turning back.

Dear Architect:

The scenario giving rise to our recommendation assumes that the architect has reasonable grounds to believe that the owner is turning a blind eye to the “life safety” issue. Further, the scenario contemplates that the architect knows, or ought to know, that should the “life safety” issue not be addressed, it could pose a serious risk to the public. Under these circumstances, for the reasons given in the article, it is prudent to take some action. We stress that the steps suggested in the article should not be taken lightly. If you encounter this situation, we strongly encourage that you contact Pro-Demnity or consult legal counsel.

Kind Regards,

Andrew Lundy

Partner, Brunner and Lundy

Our Contributors

Mario Delgado has developed a litigation practice in the areas of insurance defence, professional negligence (including disciplinary proceedings) and construction law. A significant portion of Mario’s practice is focused on architects and other design professionals. He is regularly engaged in construction disputes and claims including errors and omissions in design, bidding and tendering, fee disputes, product liability and delay claims.

Mario can be contacted at:

Brunner and Lundy

360 Bay Street, Toronto, ON M5H 2V6

Telephone: (416) 966-9955

brunnerandlundy.com

Rachel Migicovsky is a litigation lawyer at Shibley Righton LLP. She practices in a variety of areas, focusing on construction law and professional liability. She is originally from Ottawa, and attended Osgoode Hall from 2009–2012. She was called to the bar in 2013. Rachel serves on the executive committees of the Ontario Bar Association’s Civil Litigation section and Women Lawyers’ Forum.

Rachel may be reached at:

Shibley Righton LLP

250 University Avenue, Toronto, ON M5H 3E5

Telephone: (416) 214-5200

shibleyrighton.com

The Straight Line is a newsletter for architects and others interested in the profession. It is published by Pro-Demnity Insurance Company to provide a forum for discussion of a broad range of issues affecting architects and their professional liability insurance.

Publisher: Pro-Demnity Insurance Company

Editor: Gordon S. Grice

Design: Finesilver Design + Communications

Address: The Straight Line c/o Pro-Demnity Insurance Company 160 Bloor Street East, Suite1001, Toronto, ON M4W 1B9

Contact: mail@prodemnity.com

Pro-Demnity Insurance Company is a wholly owned subsidiary of the Ontario Association of Architects. Together with its predecessor the OAA Indemnity Plan, it has provided professional liability insurance to Ontario architects since 1987.

Questions related to the professional liability insurance program for Ontario architects may be directed to Pro-Demnity Insurance Company. Contact information for the various aspects of the program can be found on the Pro-Demnity website: www.prodemnity.com

Pro-Demnity Insurance Company makes no representation or warranty of any kind regarding the contents. The material presented does not establish, report or create the standard of care for Ontario architects. The information is by necessity generalized and an abridged account of the matters described. It should in no way be construed as legal or insurance advice and should not be relied on as such. Readers are cautioned to refer specific questions to their own lawyer or professional advisors. Letters appearing in the publication may be edited.

Efforts have been made to assure accuracy of any referenced material at time of publication; however, no reliance may be placed on such references. Readers must carry out their own due diligence.

This publication should not be reproduced in whole or in part in any form or by any means without written permission of Pro-Demnity Insurance Company. Please contact the publisher for permission: mail@prodemnity.com